How Long Does it Take to Build Credit?

Build strong credit

while you save

As a general rule of thumb, it takes about 3 to 6 months of payment history to build credit. Credit Strong reports payments monthly, so it takes about 3 months to see an initial impact on your credit score. On average, Credit Strong customers see an increase of more than 25 points within 3 months of opening their account. Credit Strong account holders that make all their payments on time for 12 months more than double that score increase to almost 70 points after 12 months.

Of course, everyone’s personal credit profile is different and individual results vary.

How Long Does it Take to Build Credit from Nothing?

Building credit takes time. The length of that time will vary significantly based on your credit profile. But what if you have no credit history at all?

Everyone starts with no credit profile. If you apply for a loan when you have no credit profile, your credit score will be a zero or ‘null value’ meaning you have no credit history.

Before we go into the options for establishing credit, it may be important for you to understand the basics of credit scores, so as you start building credit you can make smart credit building decisions.

When you have no credit profile at all and get your first credit card or loan from a lender that reports to the three major credit bureaus, it will take about 1 to 2 months from the date your account is reported to the bureaus to get a VantageScore® and about 6 months to get a FICO® Score.

How Long Does it Take to Get a 700 Credit Score?

A credit score of 700 or higher is a worthwhile objective because you may unlock lower interest rates on credit cards and loans, more favorable insurance terms, and better financing options. The effort required to achieve a 700 credit score depends a lot on your current credit profile. If you just have a limited credit profile with no or few accounts reported for a short duration of time it may be much easier and faster to get a 700 credit score than if you have a payment history of late payments, missed payments, bankruptcy, or collection accounts.

If you have a limited credit history, you can make rapid progress to achieve your goal by simply adding a good mix of accounts and making on-time payments. Some suggestions on how to build and improve your credit score quickly are included below, including: adding a credit builder account, obtaining a secured credit card, or reducing your credit utilization.

The strength, or weakness, of your current credit report will determine how much work and time need to be spent to get your score to 700. For example, if your credit report already has some good accounts on it and no delinquencies, then you can boost your score faster than someone with a more challenged credit history that includes foreclosures or bankruptcy for example.

FICO created a free credit score estimator to help you see what your credit score would be if you change factors in your credit profile. If you’re curious how much your score could change if you improve your credit profile, it’s worth taking a look.

How Long Does it Take to Build Credit to Buy a House?

It is hard to estimate precisely how long it will take to have a strong enough credit score to buy a house. In part, this is due to the many variables that make up your credit history. It also has to do with what type of mortgage loan you want to apply for.

The credit bureau, Experian, defines 670 as the minimum FICO score that someone should have to be considered a good credit risk for buying a house. To them, anyone with a score of less than 670 is considered a “subprime borrower”. But just because you have a credit score below 670 doesn’t mean you can’t buy a home.

Some loans are backed by government agencies or quasi-government agencies, such as the following:

- Federal Housing Administration (FHA)

- US Department of Veteran Affairs (VA)

- US Department of Agriculture (USDA)

- Conventional Mortgage Loans

- Federal National Mortgage Association (FNMA or Fannie Mae)

- Federal Home Loan Mortgage Corporation (FHLMC or Freddie Mac)

Many of these government-backed loans come with lower minimum credit score requirements.

FHA loans often have very small down payment requirements and are available to borrowers with credit scores as low as 580. With a down payment of 10% or more FHA programs can sometimes approve borrowers with credit scores as low as 500, but that’s the exception, not the rule.

VA loans are only available to borrowers that have served in the military. VA loans have a 500 minimum credit score and very low down payment requirements.

USDA loans are for rural properties. The USDA has a 580 minimum credit score requirement.

Conventional loans are the most common type of home loan. They have modest down payment requirements and offer long-term, fixed-rate loans up to 30 years. Conventional loans also have a maximum loan size. The maximum conventional loan size for 2021 is $548,250. In areas designated as “high cost areas”, the maximum loan limit can go up to $822,375. To see the largest loan size available in your area you can check on this spreadsheet from the Federal Housing Finance Agency. To obtain a conventional mortgage loan you’ll need at least a 620 credit score.

If you want to get a large home loan, often called a ‘jumbo’ home loan, you will need a credit score of at least 660.

While all of these loan types have minimum credit score requirements, the higher your credit score the better your chances for approval and you’ll get a lower interest rate on your loan.

To estimate how much you will save in interest expense by increasing your credit score you can use this Interest Savings Calculator from FICO.

Keep in mind that mortgage lenders also look at other factors from a borrower besides their credit score. For example, they also take into consideration the down payment amount and how long you have had your current job.

Besides boosting up your credit score, you’ll also want to take into consideration building an employment history of at least 12-24 months and saving a down payment.

How the FICO Credit Scoring Model Works

To understand your credit score, you need to know how your credit records are kept. There are three primary consumer credit reporting bureaus that gather and provide your credit profile information:

- TransUnion

- Equifax

- Experian

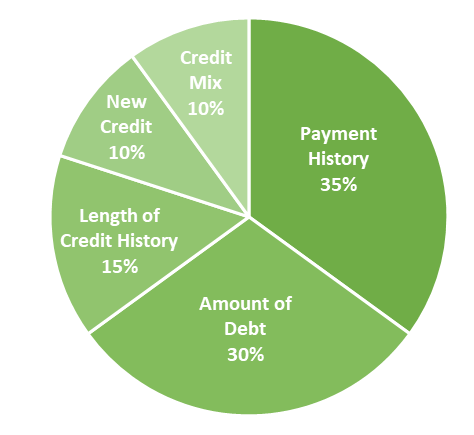

Your FICO credit score is the leading indicator of how good your credit is. It is based on credit records provided by those three credit bureaus. There are five primary factors that impact your FICO Score credit score:

- Payment History

- Amount Owed

- Length of Credit History

- Credit Mix

- New Credit

Each of these factors influences your credit score to a different degree.

Payment History (35%)

As mentioned above, payment history is the most critical factor in your credit score. Payment history accounts for 35% of your FICO credit score.

When a lender is deciding to approve or deny a credit application, it wants to know how reliable you are for making payments to repay the credit. Establishing a responsible pattern of on-time payment history is the most critical factor for building great credit.

Amount Owed (30%)

Paying on time is important. But the amount you owe is almost equally influential when it comes to calculating your credit score. The amount you owe represents 30% of your overall FICO credit score.

Credit utilization for your credit cards is the primary tool used to measure ‘Amount Owed’. Having a lower utilization amount is typically better. 1% to 9% is ideal. 10% to 30% is OK, and anything over 30% may cause your credit score to actually decrease. A low credit utilization rate implies that you are not financially dependent on the money you borrow. This is a good sign to lenders when they evaluate giving you a loan or credit card.

Coming closer to your credit limit can show that you are a higher risk borrower because it appears that you ‘need’ the credit just to make ends meet. This makes future lenders potentially more apprehensive about giving you new credit.

Length of Credit History (15%)

Credit reporting bureaus pay close attention to the length of your credit history. A longer credit history often has a positive effect on your credit file.

The length of your credit history contributes to 15% of your credit score. Credit Strong Subscribe and MAGNUM accounts allow you to build up to 120 months of payment history while giving you the option to cancel anytime for free if your financial circumstances change or you want to close the account for any other reason.

Credit Mix (10%)

Your credit mix is responsible for 10% of your FICO credit score. Credit mix refers to the different types of credit you have.

Your mix can include a revolving credit account, like credit cards and lines of credit, or installment accounts, such as car loans, home loans, student loans, personal loans, or credit builder loans.

You don’t need to have every kind of credit product to have good credit, but it helps to have a somewhat diversified mix.

However, you may not want to add to your credit mix too quickly. Applying for multiple loans or credit cards in a short time indicates to lenders that perhaps you are in financial distress and need credit just to get by. This may diminish your chances of loan approval.

New Credit (10%)

The final 10% of your FICO credit score comes down to new credit. As mentioned above, applying for too many new credit accounts in a short time frame can lead to a poor credit score. When a lender is evaluating giving you a loan or credit card, it will typically perform a ‘credit inquiry’ by asking the credit bureaus about your credit report. There are two types of credit inquiries: a ‘hard inquiry’ and a ‘soft inquiry’.

Hard credit inquiries typically include a complete credit report that includes all of your loans, credit cards, and credit utilization, along with any other factors that might impact your ability to repay, including foreclosures, bankruptcies, collections, etc. Hard inquiries can slightly lower your credit score, especially when you have a lot of them in a short time period. Hard inquiries are tied to an actual application for credit.

Soft inquiries occur when you check your own credit or when businesses, such as lenders, insurance companies, or credit card companies, check your credit to pre-approve you for offers. Soft inquiries aren’t linked to a specific application for new credit, so these inquiries have no effect on your credit score and are never considered as a factor in credit scoring models.

New credit can reduce the average age of your credit accounts. This may have a slight negative impact on your credit score in the short-term, until the new accounts begin to age, increase their payment history, and increase the length of time the account has been open.

How the FICO Credit Scoring Model Works

In most cases, getting a good credit history is the result of years of work. Yet, some people wonder if there is a way to quickly boost a credit score.

If you’re motivated to quickly increase your credit score, here are three strategies that might work for you:

- Get a secured credit card

- Get an installment loan or a credit-builder account

- Reduce your credit card utilization

Combining these three methods is one of the best ways to speed up your progress towards good credit. To get started, Credit Strong offers a credit builder loan to help you begin improving your credit profile in just 3 to 6 months.

How the FICO Credit Scoring Model Works

If you already have bad credit, don’t lose hope. There are ways to build credit even if you can’t get a credit card.

Start by taking the steps you would use to build credit fast regardless of your current situation. Then add on these credit repairing tactics:

- Immediately find and dispute any incorrect information in your credit file

- See if you can negotiate to remove collections accounts with collection agencies

- Pay down the balance on any high balance credit card accounts

Fixing bad credit can take time. The tips above will get you started and help you shorten the time it takes to get good credit.

Why Does it Take Time to Build Excellent Credit?

As we have already shown, the credit scoring models were developed to reward people who make their loan payments on time, keep low revolving credit balances, and have a long credit history.

For a person starting with no credit, building a solid payment history takes time. Time is so important that length of credit history is its own scoring factor.

But don’t get discouraged! If you’re looking to build your credit, getting started now can bring you rewards for the long term.

There’s a saying when it comes to planting trees, and it applies to credit building too. The best time to plant a tree is 10 years ago or today. The best time to start building strong credit was 10 years ago or today, so if you didn’t start 10 years ago, get started on building strong credit today!

CreditStrong helps improve your credit and can positively impact the factors that determine 90% of your FICO score.