Can I Get a Car Loan with a Credit Score of 600?

Build strong credit

while you save

You can get an auto loan with a credit score of 600. You will pay a higher interest rate than a borrower with excellent credit, but you will still be approved.

Many car lenders classify a borrower with a 600 credit score and below as “subprime” and a borrower with a score of 601 or above as “non-prime”. Getting on the upper side of that line can make a big difference.

If you have a 600 credit score, consider working to improve your credit before applying for an auto loan.

Can I Get a Car Loan with a Credit Score of 600?

A credit score of 600 is well below the average credit score of 711. For many auto lenders, it puts you on the boundary between the “subprime” and “non-prime” credit score ranges.

That means you can get a loan, but it may be a fairly expensive loan. You will get a better deal if you can raise your credit score.

What Is the Minimum Credit Score Required to Buy a Car?

It’s hard to get a loan if you have poor credit. It’s still possible for a subprime borrower to get an auto loan.

An auto car loan is a secured loan: the vehicle is collateral for the loan. If you default, the lender can repossess the car. The lender faces less risk than they would with unsecured debt, like student loans or a personal loan.

That makes lenders more willing to work with people who have poor credit or fair credit.

Experian reports that in Q2 2020, over 19% of all auto loans went to people with subprime credit (scores from 501-600). Just under 3% went to borrowers with deep subprime credit (scores from 300-500).

How Your Credit Score Affects the Interest That You Pay

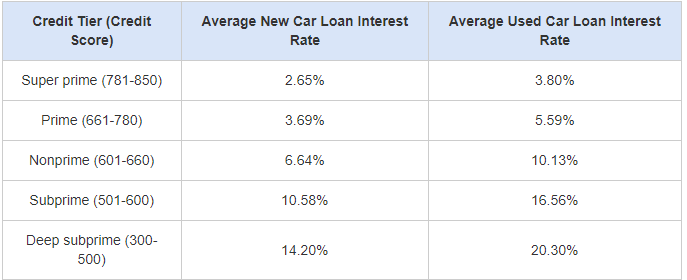

How much difference does your credit score make? Let’s look at the numbers. These are the average auto loan rates that borrowers with different credit scores will pay.

Credit Tier by Interest Rate

Source: Experian, State of the Automotive Finance Market, Q4 2020, via Cars Direct

Those rate differences translate into big savings for people with better credit. This table shows the monthly and total costs for a 60-month new car loan of $30,000 (the average US new auto loan is $34,635).

Interest Paid By Credit Tier

| Interest Rate | Monthly Payment | Total Interest Paid | Total Cost |

| 2.65% (Super prime) | $534.41 | $2,064 | $32,064 |

| 3.69% (Prime) | $548.31 | $2,898.52 | $32,898.32 |

| 6.64% (Non prime) | $588.95 | $5,337 | $35,337 |

| 10.58% (Subprime) | $644.82 | $8,689.02 | $38.689.02 |

| 14.20% (Deep Subprime) | $701.16 | $12,609.72 | $42,069.72 |

Source: Experian Auto Loan Calculator

A subprime borrower (501-600) will pay 10.58% interest and their total interest payment will be $8,689.02.

A non-prime borrower (601-660) will pay 6.64% and their total interest cost will be $5,337. That’s a difference of $3,352, and a $55 higher monthly payment!

Different lenders may use different score ranges and may make contrasting offers to a borrower with a 600 credit score.

How to Get a Loan with Bad Credit

You can find an auto loan with poor credit. Start by setting a realistic budget: lenders will be more likely to approve a bad credit auto loan if you can afford the car you want to buy. Always shop around. Getting quotes from several lenders will help you get a better deal.

Remember to try your own bank or credit union! They know your finances and you can often talk directly to decision-makers.

Consider Putting Down a Larger Down Payment

A down payment may seem like a burden, but there are good reasons to make a substantial down payment on an auto loan.

A substantial down payment will make it easier to get approved for a car loan. It will often get you a better interest rate.

A down payment will reduce your monthly payments and you’ll be less likely to experience negative equity, or owing more than your car is worth. Negative equity can make it hard to sell your car and you may need additional insurance.

Consider a Cosigner

If your credit is not good enough to get you approved for a loan or if you’re being offered very high auto financing rates, a cosigner could solve your problem. If a friend or relative with better credit cosigns your loan the lender will consider their credit score as well as yours.

If you fail to make your payments, the cosigner will be legally liable for the balance. Your cosigner’s debt-to-income ratio will also be affected. That could make it harder for the cosigner to get a mortgage or car loan.

Be sure that both you and your cosigner understand the risks and responsibilities that go with cosigning a loan.

What Credit Score is Needed to Buy a Car Without a Cosigner?

There is no cutoff point that determines when you need a cosigner to get approved for an auto loan. Different lenders have different criteria.

If you can’t get approved for a loan or if the interest rates are just too high, looking for a cosigner could be the right move.

How to Improve Your Approval Odds Before Applying for a Loan:

There are several steps that can give you a better chance of getting a loan with a 600 credit score.

Improve Your Credit Score

Taking the time to work toward a higher credit score can get you a substantially better deal on an auto loan. These steps will help you build your credit history.

Check Your Credit Reports

Many credit reports contain errors, and those errors can hurt your credit. Review your credit reports and dispute any inaccuracies.

Watch Your Payment History

Payment history is the single most important part of your credit score. If you have late payments, bring them up to date. Make every debt payment on time!

Keep Your Credit Utilization Low

Each credit card has a credit limit. The percentage of your credit limit that you actually use is your credit utilization rate. If your card limit is $1000 and your balance is $300, your credit utilization rate is 30%.

Keep your credit utilization rate under 30%. Lower is better!

Use a Credit-Builder Loan

A credit builder loan can give your credit an immediate boost, especially if you don’t have an active installment loan on your credit history. At the end of a credit-builder loan term, you’ll get a lump sum, which you can use toward your down payment.

Banks, credit unions, and online lenders, like CreditStrong, offer credit-builder loans.

Use a Secured Credit Card

If you don’t have a credit card, applying for a secured card can improve your credit mix. Be sure to use your card wisely. Keep your balance below 30% of your credit limit and make every payment on time!

Don’t Close Old Accounts

Length of credit history is a part of your credit score, and closing accounts will reduce it. Even if you’re not using an old credit card, keeping it open will extend your credit history and help your credit.

The only exception to this rule would be a credit card with a substantial annual fee.

Pay Off Balances

If you’re carrying credit card balances from month to month, try to pay them off. Lower balances mean a lower credit utilization rate. That can boost your score quickly.

Paying off balances also means you’re paying less interest. That’s always a good thing!

Ask for a Credit Limit Increase

Many credit card issuers will give you a credit limit increase if you ask for it, especially if you have a good payment record. A higher credit limit is a fast way to lower your credit utilization rate.

Don’t let a higher limit tempt you to spend more money!

Become an Authorized User

Asking a credit card user with a good record to add you as an authorized user is a quick way to help your credit history. Be sure to check whether their card issuer reports authorized users to the credit bureaus.

Use Your Bill Payments

Services like Experian Boost and eCredable Lift place your bill payments on your credit report and can boost your credit scores with the credit bureaus that offer them (Experian and TransUnion).

Any of these steps can help bump your credit score up. Using several of them at the same time can give you better results.

All of these methods will have a greater and faster impact if you have a relatively thin credit file. The more information there is in your credit report, the more new information it takes to move your score.

Try to Get a Preapproved Loan

Many lenders offer preapproval. A preapproved loan is a non-binding agreement to lend an estimated amount with estimated terms. It’s not final but it gives you a good idea of what your loan terms will be.

Getting preapproved has significant advantages.

- Negotiating power. If you have a preapproval in hand you’re in a better position to negotiate with a car dealer or another lender.

- You’ll know what you can spend. A preapproval will give you the maximum amount you can borrow. That will help you choose an appropriate car.

- You’ll avoid upsells. It’s harder for a dealer to pitch expensive modifications if you can only spend a fixed amount.

A preapproval is not a final commitment, but in most cases, it will be close to the final terms you are offered.

Getting preapproved by several financial institutions will allow you to compare offers. Try your bank or credit union, online lenders, and online loan brokers.

Pay a Higher Down Payment

There are multiple advantages to making a higher down payment.

- You’re more likely to be approved.

- You’ll probably get a better interest rate.

- You will have lower monthly payments.

- You’re less likely to be underwater on your loan (owing more than the car is worth).

Putting the cash together for a large down payment can be a struggle, but the benefits are worth it.

Consider a Lease

Can you lease a car with bad credit? Yes, you can.

Many people criticize leasing because you don’t build up equity. If you take out a long-term loan with a low down payment, you won’t have much equity even with a purchase. You may even owe more than the car is worth for much of your loan term.

If you lease with bad credit, you will not get the best terms. You may have to shop around for a dealer willing to lease you a car. You may also have to pay a higher down payment and monthly payment than you’d like. But it could still be a better deal than a bad credit car loan.

Make the Right Choice

What is a good credit score to buy a car? A higher credit score will get you lower interest rates. If your credit score has taken some damage, you can still buy a car. You will just have to pay more for your auto loan.

A low credit score is not just an obstacle to getting what you want. It’s also a warning. The companies who calculate your score aren’t out to get you. They are objectively assessing the probability that you’ll default. A low score means your risk of default is high.

Default isn’t just bad for the lender. It’s also bad for you. If you default, your car could be repossessed and your credit could get a whole lot worse.

If your credit score isn’t great, let that warning work for you. Improve your finances and your credit report before taking on more debt. You might want to drive your old car a little longer or delay buying your first car while you get your financial house in order.

That might not be the choice you want, but it could be the choice you need!

CreditStrong helps improve your credit and can positively impact the factors that determine 90% of your FICO score.